This $28 Million Ether Market Bet Aims to Profit From Pure Market Chaos

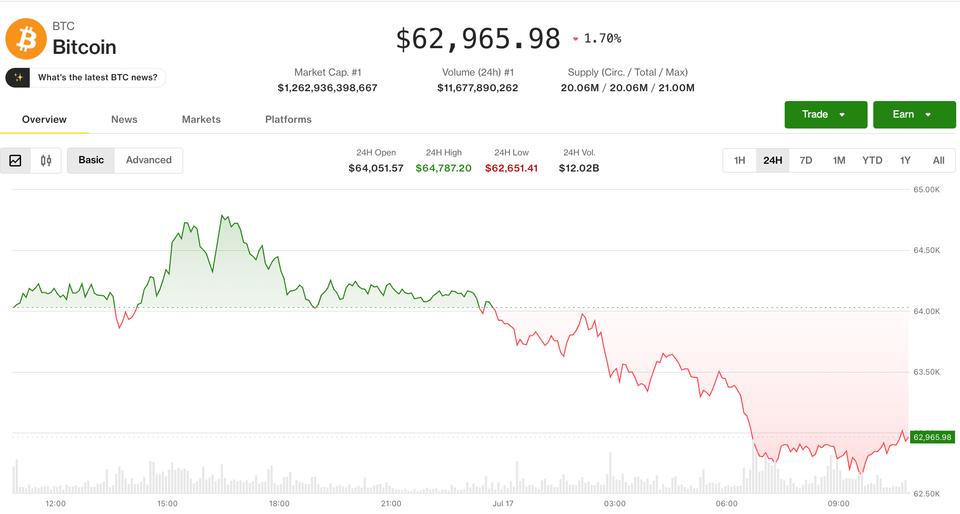

A trader has placed a $28 million bet on Ether (ETH) volatility, buying both calls and puts at a $1,875 strike price expiring July 24. This straddle strategy profits from significant price swings in either direction.

Intelligence analysis by Gemini 2.5 Flash Lite

A substantial $28 million trade on Ether is betting on extreme price volatility by July 24. The trader simultaneously bought call and put options, aiming to profit from a large upward or downward price movement, treating volatility itself as a tradable asset.

Imagine someone betting that a bouncy ball will either go super high or super low, but they don't know which. They pay a little money for two "tickets": one wins if it goes high, and one wins if it goes low. If the ball moves a lot, they win money, but if it just sits there, they lose the money they paid for the tickets.

Analysis

A Volatility Play on Ether

The recent $28 million "long straddle" trade on Ether represents a significant bet on market turbulence rather than a directional price forecast. By simultaneously purchasing 7,500 call options and 7,500 put options at a $1,875 strike price, with an expiration date of July 24, the trader is positioning to capitalize on substantial price swings in either direction. This strategy is akin to hedging against uncertainty, where the profit is derived from the magnitude of price movement, not its specific trajectory. The trader paid a premium of $852,000 for this position, which constitutes the maximum loss if Ether remains relatively stable until expiry.

Treating Volatility as an Asset

This trade underscores a sophisticated approach to market speculation, where volatility itself is treated as a separate asset class. The trader is not necessarily predicting whether Ether will rise or fall, but rather that it will move significantly. This strategy leverages options "Greeks" like vega (sensitivity to volatility) and gamma (sensitivity to price acceleration) to extract value from market choppiness. It signifies a departure from simple "long-only" or "short-only" positions, indicating a maturing derivatives market that offers tools for more complex risk management and profit generation strategies.

The Risks and Rewards of Straddles

While the potential profit from a straddle is theoretically unlimited, as asset prices can move dramatically, the strategy is fraught with peril. The primary risks include the cost of the premium paid and the relentless erosion of option value due to time decay. If Ether's price remains within a narrow range until the July 24 expiry, the entire $852,000 premium could be lost. Executing such a trade requires a deep understanding of options mechanics, risk management, and the ability to navigate the complex interplay of market forces that drive volatility. Without professional-grade expertise, capital can be rapidly depleted.

Key points

- A trader placed a $28 million notional long straddle on Ether (ETH).

- The trade involves buying 7,500 call and 7,500 put options at a $1,875 strike, expiring July 24.

- This strategy aims to profit from significant price volatility in Ether, regardless of direction.

- The maximum loss is the $852,000 premium paid if Ether remains range-bound.

- The trade highlights volatility as a tradable asset class in crypto markets.

If Ether experiences significant price volatility before July 24, this straddle position could yield substantial profits for the trader. The strategy is designed to benefit from unexpected market events or sharp trend reversals, turning turbulence into gains.

The primary risk is that Ether's price remains relatively stable until the July 24 expiry. In this scenario, the $852,000 premium paid for the options would be lost due to time decay, representing the maximum downside for the trade.